Investing: Is it skill or luck?

Investing: Is it skill or luck?

Losing On Purpose in Skilled Games

From time to time, we contemplate deeply about the drivers behind our own investing performance and sometimes that of others (so we know who is worth learning from), so as to determine if one’s out-performance is attributed more to skill or luck.

Thus when I chanced upon this quote below by Michael Mauboussin in his book “The Success Equation”, it sparked this article.

“There’s a quick and easy way to test whether an activity involves skill: ask whether you can lose on purpose.

In games of skill, it’s clear that you can lose intentionally, but when playing roulette or the lottery, you can’t lose on purpose.”

— Michael Mauboussin

With activities of skill, like chess, swimming, basketball, one can lose on purpose (as long as you have some basic mastery of the activity).

Whereas with activities of luck, like roulette, coin toss, lottery, one cannot lose on purpose. If one cannot lose on purpose, one cannot win on purpose.

Following which, if one can lose on purpose, one too can win on purpose, it is likely to be an activity of skill.

This has significant implications to us as investors, who are buyers of individual stocks for the long-term.

Can this similarly be applied to investing? Which begs the question, can one lose intentionally and pick losing stocks for the long-term?

Understanding Luck

Luck is a chance occurrence that affects a person or a group. It can be good or bad. But luck is out of one’s control and is unpredictable. Scores of games where luck is significant, then becomes an imprecise measure.

Randomness and luck are related, but there is a useful distinction between the two. Randomness is operating at the level of a system (base rate), but luck is operating at the level of the individual.

Play a fair coin toss, and there’s a 50–50 chance of heads and tails each time with the same loss/gain payoff. Each toss is an independent outcome that operates at the individual level.

One can be lucky and make ten consecutive right guesses and be an outlier winner (in the short-term), but that does not necessarily make one a good coin guesser. It is crucial to distinguish between luck and skill.

But eventually if the game is played many times enough (in the long-term, think 10,000 and more), the average probability of winning/losing eventually gravitates towards the system-level base rate (~50%).

Thus with sufficient sample sizes, it is crucial to understand and differentiate that for each activity/game, if one is an outlier winner more because of luck or skill.

Understanding Skill

Skill is best defined as a one’s ability to use their knowledge effectively and readily in execution or performance. Skill can be acquired through the deliberate practice of physical or cognitive tasks.

Skill is best defined as a process of making decisions.

“When luck has little influence, a good process will always have a good outcome.

When a measure of luck is involved, a good process will have a good outcome but only over time.”

— Michael Mauboussin

There are typically Three Stages of Acquiring a Skill

Cognitive stage: You try to understand the activity and you make a lot of errors. It is generally the shortest.

Associative stage: Your performance improves noticeably and you make fewer errors that are more easily corrected.

Autonomous stage: The skill becomes habitual and fluid.

Improving a Skill usually boils down to deliberate practice.

Repetition: It involves hours of concentrated and dedicated repetition.

Feedback: Deliberate practice also requires timely and accurate feedback.

Effort: Deliberate practice is laborious, time-consuming, and not much fun, which is why so few people become true experts or true champions.

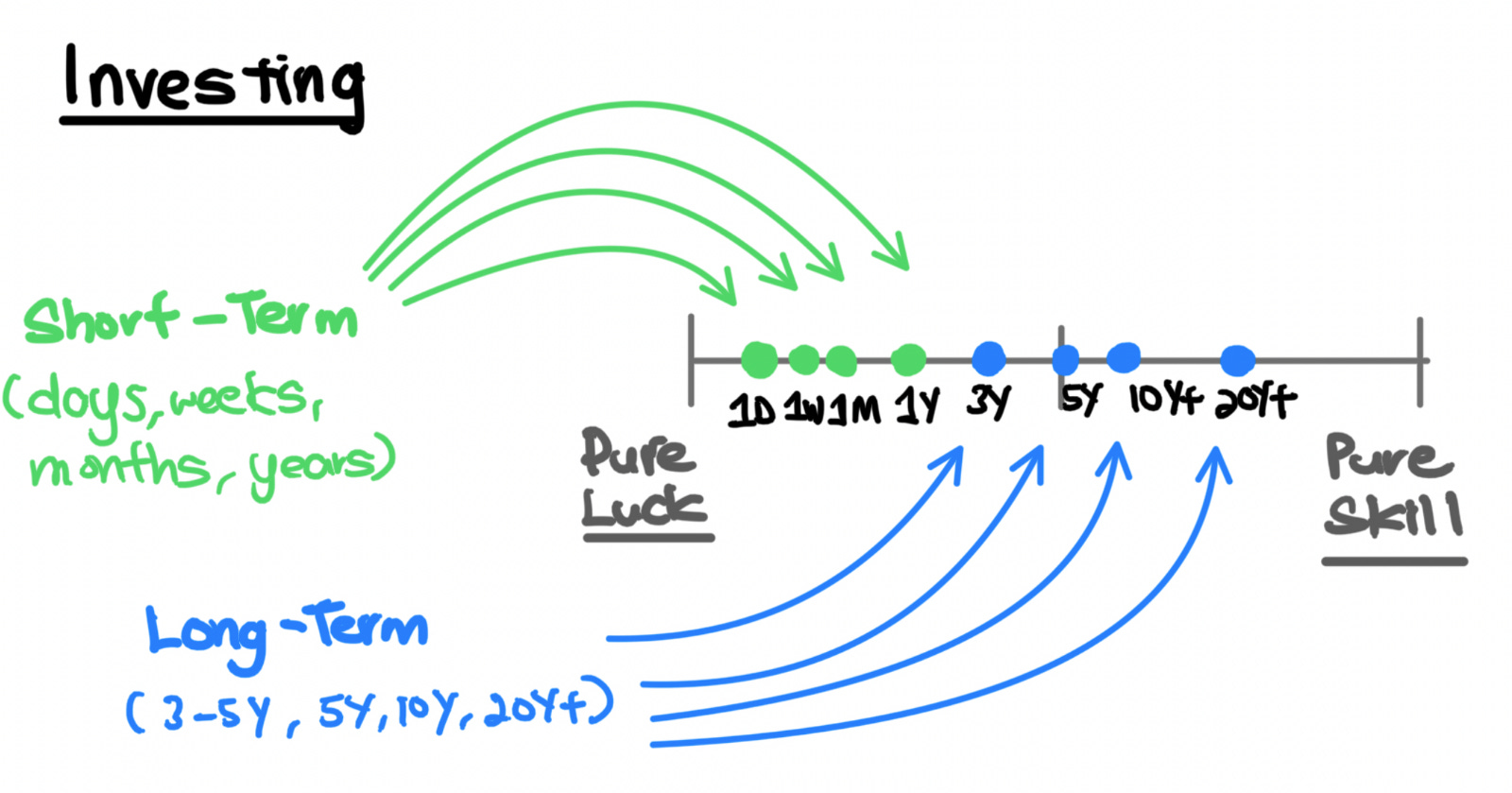

The Luck-Skill Continuum

It is important to differentiate an activity if it is skilled or unskilled, and the interplay between luck and skill. More specifically where the activity itself sits in the luck-skill continuum, and also consider the time perspective, if it is to remain static or improve or deteriorate with time.

Far left | Pure Luck, No skill: Cause and effect poorly correlated in the short run, good and bad decisions can lead to success.

Far right | Pure Skill, No Luck: Clear, accurate feedback, close relationship between cause and effect.

Interestingly, amongst sports and activities ranging from like almost pure-skill games like chess and almost pure-luck games like roulette, Michael Mauboussin postulates in his book (that investing is far more a game of luck than skill.

Instead, we like to push the thinking further.

What Drives the Stock Market Returns?

In the near-term, Mr Market is a noisy, emotional and irrational voting machine, driven by revenue/earnings expectations, interest rates movements, risk uncertainty, sentiment & psychological factors like optimism, pessimism, fear & greed.

In the long-term, Mr Market is a far less irrational weighing machine, the rising stock market is supported by rising earnings.

In the short-term (i.e. 1 year), it is the expansion of valuation multiples that drive most (~46%) of stock market returns.

But in the long-term (i.e. 10 year), overwhelmingly it is the growth of sales and profits (~89%) that drives the majority of stock market returns.

It is important to understand what drives stock market movements in the short-term (noise, volatility) and what truly drives stock market movements in the long-term (growth of sales, earnings, and cash flows).

Investing: Skill vs Luck

That is also, why we are of the following view that:

Investing, especially over relatively short periods of time, is much more a matter of luck than of skill.

Investing, especially over relatively long periods of time, is much more a matter of skill than of luck.

Investing is often viewed by many and the financial media as more luck than skill, because in the short-term, feedback loops are often unclear and inconsistent and can be very volatile.

In addition, very few investors keep playing the game very well for decades and beyond, thus investing is rarely viewed as a skilled game by most.

But as we think one can possibly win intentionally (read our book to find out how), we do believe one can also lose intentionally as well.

To us, investing is both a game of both luck and skill, and where it is on the continuum, depends on the strategy deployed, how it is being played, and the time perspective.

“Professionals win points; amateurs lose points.” — Dr Simon Ramo

We do believe that gradually with time, in years and decades, that investing as an activity in the luck-skill continuum, can shift more to the right over time (i.e. more skill than luck), as skill becomes more evident for the ones who do have the skill, with luck still playing a crucial role.

“While I much prefer a five-year test, I feel three years is an absolute minimum for judging performance. It is a certainty that we will have years when the partnership performance is poorer, perhaps substantially so, than the [market]. If any three-year or longer period produces poor results, we all should start looking around for other places to have our money. An exception to the latter would be three years covering a speculative explosion in a bull market.”

— Warren Buffet, Buffett Partnership 1962 Annual Letter

Losing on Purpose in Investing

There are many ways to lose intentionally in investing, to under-perform the market and could even get wiped out. The focus is on payoffs whose downside is unlimited. Thus when something goes bad, it goes really bad, and one can be wiped out, and cannot recover from it.

Here are some ways, which one might do okay in the first few periods, but can then be wiped out eventually:

Go short on a single stock (one of my high conviction longs) with the entire portfolio’s capital with maximum leverage.

Sell naked call options on a single stock with the largest possible position, that has no subsequent long position.

Vice versa, sell naked put options on a single stock with a largest possible position, that you no longer have capital to buy.

Keep trading in an out of a single stock many times a day. It is not the market returns will drag you, but the transaction costs from the incessant trading over years that will pile up and drag the performance.

All either incorporate leverage, high concentration, and/or have some form of unlimited downside/limited upside payoffs (see below).

Ultimate success is not defined by the frequency of gains, but rather by how much you make when you are right versus how much you lose when you are wrong.

Making It More Difficult to Lose

Since it can be quite easy to get wiped out fairly quickly. Let’s make the game of losing purposely in investing a little tougher:

The use of leverage is not allowed.

Trading is not allowed. Only buy and hold single-name stocks.

The use of shorts, and options or any derivatives are not allowed.

Concentration is not allowed.

Portfolio must have at least 20 stocks and allocation equal-weighted.

Applicable to US-listed companies with a market cap of at least US$1 billion (as of 1 Jan 2022) only.

Performance will be measured annually and ends after 5 years.

Some Traits that We Generally Avoid

❌ Near perfectly competitive businesses with low competitive advantages, with little to no moat, not top dog, losing market share.

❌ Companies that are structural declining for the mid to long-term.

❌ Experience slowing or rapidly declining revenues, poor quality of revenues, and non-recurring in nature.

❌ Poor customer satisfaction, low NPS scores, torrid product/service reviews.

❌ Capital intensive businesses, require a lot of CAPEX, high payback periods.

❌ Poor unit economics, high CAC to LTV (low CAC or high LTV), low gross profit margins.

❌ Profitable / Not profitable with structurally deteriorating profit and cash flow margins.

❌ High debt to cash levels, high net debt levels relative to capital structure.

❌ Inept management, unhappy employees, low GlassDoor ratings.

Trying to Lose on Purpose

Investing is neither a pure game of skill or a pure game of luck. Investing instead, is a game of both skill and luck.

We believe that through this challenge below, we might uncover more skilled investors hiding amongst us than financial media makes us think otherwise.

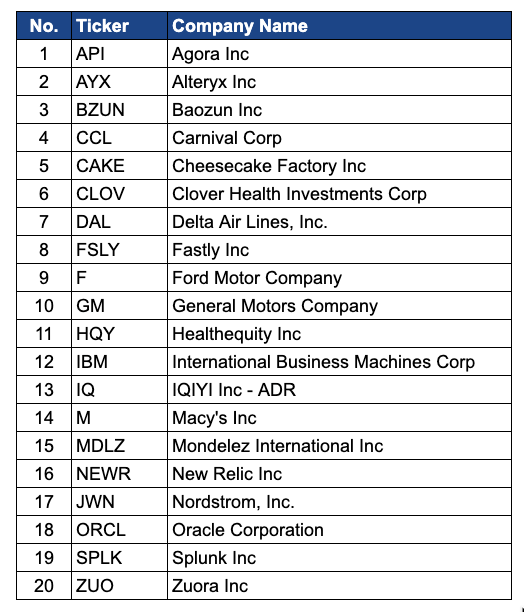

Below is the list of 20 companies (in ascending alphabetical order) that we think, as a portfolio of equally-weighted positions will under-perform the S&P 500 over the next 5 years and beyond. We will be tracking it annually from 1 Jan 2022 for the next 5 years to 1 Jan 2027.

Take up This Challenge!

If you are already a skilled stock picker in picking winning companies, we hope you can join us in this challenge to pick losing companies.

You can submit your list of all 20 companies (only google finance tickers needed) before 31 Dec 2021, via the link here.

E.g. AMZN for Amazon.com, Inc., AAPL for Apple Inc, etc.

Choice of any 20 publicly listed companies in the US.

Market capitalisation of at least US$1 billion (as of 1 Jan 2022).

13 Dec 2021 | Eugene Ng | Vision Capital Fund | eugene.ng@visioncapitalfund.co

Find out more about Vision Capital Fund.

You can read my prior Annual Letters for Vision Capital here. If you like to learn more about my new journey with Vision Capital Fund, please email me.

Follow me on Twitter/X @EugeneNg_VCap

Check out our book on Investing, “Vision Investing: How We Beat Wall Street & You Can, Too”. We truly believe the individual investor can beat the market over the long run. The book chronicles our entire investment approach. It explains why we invest the way we do, how we invest, what we look out for in the companies, where we find them, and when we invest in them. It is available for purchase via Amazon, currently available in two formats: Paperback and eBook.

Join my email list for more investing insights. Note that it tends to be ad hoc and infrequent, as we aim to write timeless, not timely, content.