The advantage of being a global investor located in Asia

It can actually be more advantageous than one might think.

At Vision Capital Fund, we often get these two questions from potential investors:

We see that you invest in many US stocks. Do you stay up late, monitor them, and do a lot of trading into the late hours?

Given your global investment mandate, you seemingly invest in many US stocks. Since you are geographically based in Asia/Singapore, what is your competitive advantage over US-based investors?

Let us use these two questions to frame our response.

Vision Capital Fund seeks to invest in exceptional stocks globally. We predominantly operate out of Asia/Singapore.

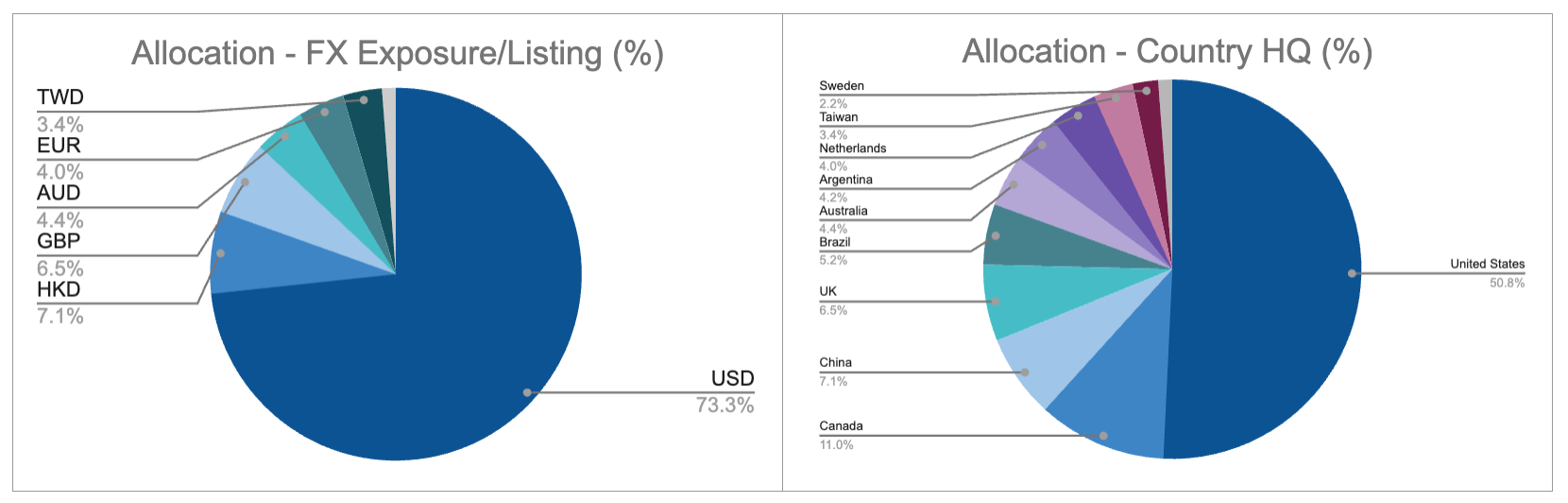

As of 31 Jan 2025, 73.3% of the Vision Capital Fund’s holdings are invested in US-listed public equities, but only 50.8% are companies with US headquarters.

Thus, while we might be perceived as primarily “US investors,” we are not. For context, the MSCI World’s country weights for the US as of 31 Jan 2025 are much higher at 73.6%.

There is a conventional opinion that investors should attempt to make money by buying low and selling high and constantly trying to find such repeat opportunities. We do not fault one for having such a popular viewpoint.

We are predominantly buy-and-hold investors, not traders who consistently attempt to buy low and sell high. We are not trying to buy a $1 coin for 60-70 cents and sell when it reaches 80-90+ cents, but we are instead trying to find high-quality $1 coins, be willing to pay $1.30-1.50 for it that we think can grow to become $10 notes.

One can play many games in the investment/trading world, and we prefer to play the long and patient one with lower transaction costs to find infrequent new investment ideas rather than engage in frequent activity that requires higher costs.

We expect our investment holding periods to be much longer, ideally in years, if not decades, than the average investor's, which has declined since the 1970s. Our portfolio turnover thus far has been zero, and we expect it to remain low.

We do our best to make excellent buy decisions so that we can make fewer horrible sell decisions. We take time to do the analytical work and make all investment decisions of what and how much to buy before the markets open.

When the markets open, we typically buy at the prevailing prices using market orders. We do not use orders. We do not care if the price is 1-2% more expensive or if we are trying to buy it 1-2% cheaper.

Because we are looking for 5-25X+ multi-baggers, the penny-pinching, pound-foolish activity of trying to time and wait to buy something slightly cheaper (and often not getting to do so) is a silly endeavor from our perspective.

We are not short-term traders or speculators, so we are not constantly glued to the computer screen, looking at price and volume charts with technical patterns, trying to time our perfect buy/sell entry. No one consistently gets it perfect; no one can buy low and keep selling high consistently—at least, I don't know anyone.

Instead, we are long-term investors who invest in companies and people. We spend a lot of time studying companies, what products and services they sell, the creation and innovation process, how they sell, what value they provide, and whether customers will keep buying and paying more for them over time. We also focus on how much profits can be made and reinvestment is needed to keep growing, the quality of the management, its strategy, execution, and culture to keep sustain the growth, and how big the market is for the company to be able to keep growing for a long time and if it can allow them to dominate for a long time.

Being based in Asia/Singapore provides a time zone and psychological behavioral advantage over our Western-based counterparts. We are nicely asleep in la-la-land when the US markets are actively trading. We typically sleep when markets open and wake up just after markets close. If we have to keep monitoring the markets, we probably are doing something wrong.

We never have to rush and make decisions when prices are constantly moving. We don’t need to check where the markets are every minute or hour because the markets are closed. As a result, we aren’t stressed by the noise. We get to focus, allowing us to do the work that truly matters.

During the Asian hours, when the US markets are closed, we do our investment research, analysis, and allocation work. This provides a serenity of peace that allows us to make decisions without countless noise and being forced to react constantly.

Being geographically located in Asia and neutral Singapore, we are indoctrinated to consider both holistic perspectives of the West and the East. We must consider both sides and the nuanced historical, cultural, strategic, and political angles.

If we were geographically located in the West, we would probably be constantly bombarded by more biased market noise, which could heavily influence and cloud our opinions, judgments, and biases. By operating out from Asia, we can set ourselves aside to ignore these noises and focus on the longer run and what is more unlikely to change.

Our guiding principle is that we prefer to have loosely held strong opinions. Should the facts change, our opinions must change and dynamically evolve accordingly. There is nothing in it for us to be stubborn or dogmatic about.

In short, being a global investor operating out of Asia/Singapore might yield far more advantages than disadvantages than one might think.

08 February 2025 | Eugene Ng | Vision Capital Fund | eugene.ng@visioncapitalfund.co

Find out more about Vision Capital Fund.

You can read our annual letters for Vision Capital Fund.

Check out our book on Investing, Vision Investing: How We Beat Wall Street & You Can, Too. We believe the individual investor can beat the market over the long run. The book chronicles our entire investment approach. It explains why we invest the way we do, how we invest, what we look out for in companies, where we find them, and when we invest in them. It is available via Amazon in two formats: paperback and eBook.

Join our email list for more investing insights. Our emails tend to be ad hoc and infrequent, as we aim to write timeless, not timely, content.

Legatum’s CIO in Dubai reference the same points.

https://youtu.be/fxVXHVgbwhU?feature=shared